Being self-employed doesn’t mean you can’t get a mortgage, and it doesn’t mean that you have to pay higher rates! It just means you will have to jump through a few more hoops and provide more evidence to the lender. If you are considering getting a new mortgage or need to renew your existing mortgage within the next few years this article is a MUST read. It contains everything you must do and not do to increase your chances of approval. The earlier you start preparing yourself, the better!

What defines you as self-employed?

Owning your own business! You can be a Sole trader without a limited company, the Director of a limited company, a Construction Scheme Contractor (CIS) or a Limited Liability Partnership (LLP). It is important to note that even if you pay yourself a salary, if you are a Director of a company with a share holding of over 25%, a lender will still categorise you as self employed and not employed.

How long do you have to be self-employed to get a mortgage?

Most lenders will require you to provide two years of income proof in the form of limited company accounts or HMRC SA302 Tax Calculations. But if you haven’t been self-employed for that long, it is still possible to get a mortgage with one years figures. It may help if before you were self-employed, you were employed in a similar role to what you are now.

What will I need to provide to get a self-employed mortgage?

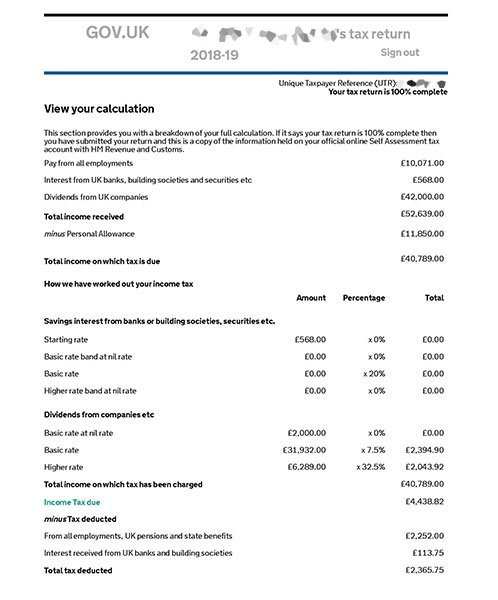

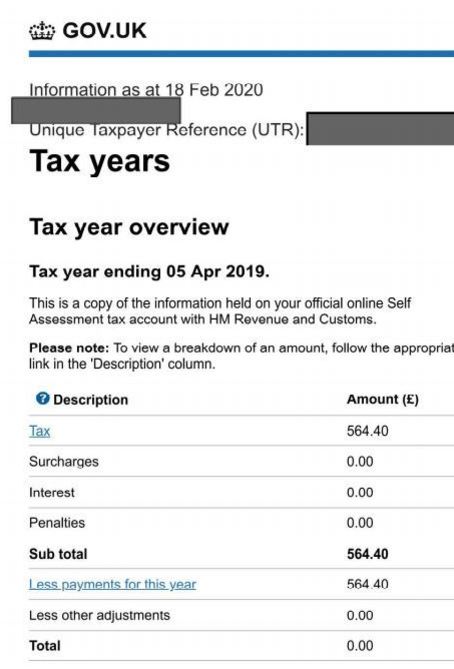

- If you are a sole trader – SA302 or Tax Calculation forms AND corresponding tax year overviews from HMRC for the last two years. See below example images of what these look like.

- If you are a limited company – Two years of certified limited company accounts – ideally these should be prepared by a qualified accountant AND SA302 or Tax Calculation forms AND corresponding tax year overviews from HMRC for the last two years.

- Business bank statements – lenders will be looking through your business bank statements to make sure that you manage your money well and the same level of income is being received as declared on your tax calculation.

- Get an accountant – Lenders don’t want to just take your word for it when it comes to your earnings. If you have a qualified accountant prepare your accounts your application will carry a lot more strength.

What self-employment income will a lender use for a mortgage?

If you are a sole trader the majority of lenders will use the ‘total income received’ figure detailed on your most recent two years SA302 tax calculation (see example image above). They then take an average from those two years figures. So if your current years income is higher, but your previous years income is lower this will reduce the income figure that lenders will look to use in their affordability calculations. There are a few lenders that may consider using the latest years income figure if it is higher than the previous years, but why limit your choice of lenders from hundreds down to just a few.

If you have a limited company, lenders will look to use your share of net profit plus salary, or your salary and dividends – as long as there is enough net profit in the company to justify paying yourself the declared amount of salary and dividends. .

If you’re a contractor, lenders will take the average of your income over the last few years. If your earnings vary dramatically, they may take your lowest earning year as a baseline for what you can afford to borrow. Some lenders may be willing to take an annualised figure from your day rate. If you are a contractor, you may also need to show evidence that you have upcoming contracts.

Things a lender DOES NOT want to see when you are self-employed applying for a mortgage

- Your accountant doing too good a job of minimising your income in order to reduce your tax bill! The lower your income, the smaller your profit, the smaller your available mortgage loan amount will be.

- A decline in declared income – the latest years ‘total income received’ on your SA302 tax calculation being less than the previous year. Lenders prefer the reassurance of knowing that your business growth is either stable or on the up.

- The net profit of a limited company being less than the salary and dividends declared on your SA302 tax calculation – you cannot pay yourself an income if there is not enough profit in the company paying you.

- Any recent change in the structure of your business for example going from a sole trader to a limited company and vice versa. Remember lenders are looking to see two years worth of limited company accounts and SA302 tax calculations. If you suddenly become the director of a newly incorporated limited company it may be difficult to convince a mortgage lender of your income and the lender may insist on two years accounts.

- Business bank statements not showing the same level of monthly income as declared on your accounts or SA302 Tax calculations.

- Significant amounts of unsecured debt such as credit card balances and personal loans.

How to find the best mortgage deals if you are self-employed

It is always a good idea to use a mortgage broker that specialises in self-employment mortgages such as myself. I have a lifetimes experience of owning businesses and have always been successful arranging mortgages for myself and other self-employed applicants, even in the most challenging situations. I know the market well and know which lenders are likely to accept a self-employed application, so I can help you find the best possible deal. beth@bemortgages.co.uk 07903 536007

6th April 2024 – HMRC is now open to the submission of new tax returns

Lenders are still allowing you to use the income from your year end 5th April 2025 tax calculations SA302 but if the figures are a little low and your business is growing and your levels of income have increased then it may be a great idea to submit your new tax return now which you can do from 6th April 2026. If you are considering getting a new mortgage or need to renew your existing mortgage within the next few years make sure you declare enough income on your tax documents!